For physicians, income protection is not an abstract concept. It is a core part of long-term financial stability. Years of education, training, and specialization mean that a doctor’s earning ability is one of their most valuable assets. If illness, injury, or burnout interrupts that ability, the financial consequences can be significant without the right safeguards in place.

Understanding what is disability insurance is essential for doctors planning their financial future. At its simplest, disability insurance replaces a portion of income when you are unable to work due to a qualifying medical condition. For physicians, however, policy structure matters just as much as the benefit itself.

As 2026 approaches, the disability insurance landscape continues to offer strong options tailored specifically to medical professionals. Knowing how these policies work, and which companies consistently serve physicians well, can help you make informed decisions.

Why disability planning is different for doctors

Many physicians assume employer-provided coverage is enough. While group plans are common, they often come with limitations. Benefits may be capped, definitions of disability may be restrictive, and coverage may not reflect a physician’s specialty or income growth.

Physicians should also review how income protection integrates with tax-advantaged tools like updated HSA contribution limits, which play a role in overall risk management planning.

This is why individual disability insurance for doctors plays such a critical role. These policies are designed to account for the physical, cognitive, and emotional demands of medical practice, especially in procedural or highly specialized fields.

Physicians typically evaluate multiple layers of protection. Short-term disability insurance and temporary disability insurance can help during brief recovery periods. However, the cornerstone for most doctors is long-term disability insurance, which provides sustained income protection for extended or permanent disabilities.

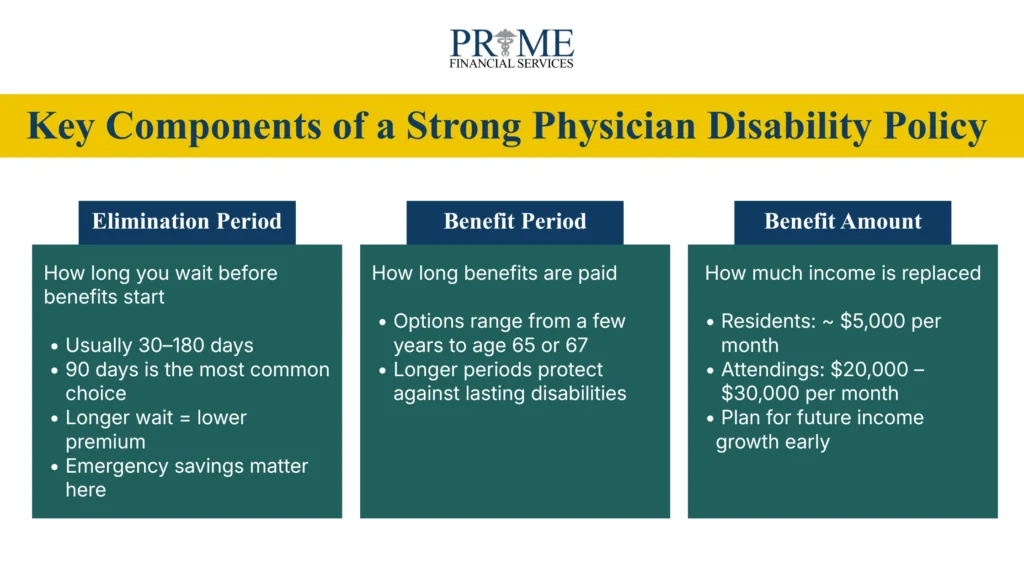

Key components of a strong physician disability policy

A well-structured policy is built intentionally, with attention to several core elements.

- Elimination period:

This is the waiting period before benefits begin. Common options range from 30 to 180 days, with many physicians selecting 90 days. A longer elimination period lowers premiums but requires sufficient emergency savings.

- Benefit period:

This determines how long benefits are paid once a claim begins. While shorter benefit periods reduce cost, most physicians choose coverage lasting to age 65 or 67 to guard against long-lasting or irreversible conditions.

- Benefit amount:

Benefit limits vary by career stage. Residents may qualify for around $5,000 per month, while attending physicians can often secure $20,000 to $30,000 per month across carriers. Planning for future income growth is critical, especially early in a career.

The importance of true own-occupation coverage

For physicians, true own-occupation language is one of the most important policy features. This definition allows benefits to be paid if you cannot perform the material and substantial duties of your specific medical specialty, even if you can earn income in another role.

All major physician-focused carriers offer true own-occupation definitions, though the exact language and specialty recognition can vary by state and carrier. This distinction protects the value of specialized training and professional focus.

Riders physicians should evaluate carefully

Optional riders often determine how well a policy performs in real-world scenarios.

- Partial or residual disability riders provide benefits when income declines due to reduced capacity rather than total inability to work. Since many disabilities develop gradually, this rider is widely considered essential.

- Recovery benefits help support physicians whose income takes time to rebound after returning to work, particularly practice owners.

- Cost of Living Adjustment (COLA) riders increase benefits during a long-term claim to help maintain purchasing power as expenses rise.

- Future increase options allow physicians to raise benefit amounts later without new medical underwriting. These riders are especially valuable for residents and early-career doctors anticipating income growth.

Mental health coverage is another critical consideration. Burnout, anxiety, and depression are increasingly common in medicine. While most leading carriers now offer extended mental health benefits, certain specialties and states may face mandatory limitations. Reviewing this provision carefully is essential.

Best disability insurance companies for doctors in 2026

When evaluating carriers, five companies consistently stand out for physicians:

- Ameritas

- Guardian

- MassMutual

- Principal

- The Standard

These carriers offer strong financial backing, physician-specific contract language, and a range of rider options. Differences exist in pricing, specialty definitions, and optional features, making personalized policy design important.

Cost expectations and common questions

A frequent question is whether disability insurance is worth it for a physician. Statistically, disabilities are more common than many expect during working years. Premiums for comprehensive coverage typically range from 3% to 5% of gross income, depending on age, specialty, and policy design.

Because disability benefits and premiums can affect taxable income differently depending on how coverage is structured, understanding the 2026 tax brackets for physicians is an important part of proper planning.

Questions about state disability programs, such as how much Louisiana pays for disability, often arise. These programs provide limited benefits and are not designed to replace a physician’s income long term. Similarly, liability coverage addresses legal risk, not income replacement.

Final thoughts

Disability insurance helps you plan responsibly for the income you have worked years to build. For physicians, the right policy structure matters as much as the carrier itself. In 2026, the best disability insurance plan is one that reflects your specialty, career trajectory, and long-term financial goals. Coordinating income protection with updated IRA contribution limits ensures retirement planning stays on track even if health interruptions occur. Thoughtful planning today can protect far more than income tomorrow.

For more than 70+ years, Prime Financial Services has specialized in helping medical professionals plan through every stage of their careers. As a third-generation firm, they integrate insurance planning with tax strategy, debt management, investments, retirement planning, and business creation.

We are committed to financial education, including seminars for residency programs, fellowship programs, and private practices nationwide, addressing gaps often left by traditional medical training.