For most physicians, taxes are not just a once-a-year headache. They are an ongoing part of a much bigger financial picture that includes student loans, practice income, investments, and long-term planning. By the time 2026 arrives, understanding how tax credits work could make a noticeable difference to your cash flow and plans. The challenge is not that opportunities do not exist. It is that many doctors are too busy caring for patients to fully understand what applies to them.

This blog breaks down what doctors need to know, what often gets missed, and how thoughtful planning can help you keep more of what you earn.

Why tax credits matter more than deductions

Many physicians are familiar with deductions because they reduce taxable income. Credits, on the other hand, reduce the actual tax bill dollar for dollar. That is why Tax Credits often have a stronger impact, especially for high-income professionals with complex financial lives.

As policies evolve, staying informed becomes critical. Annual threshold changes and phaseouts are often influenced by updated IRS 2026 inflation adjustments, which can directly impact eligibility for certain credits. Some credits phase out at higher income levels, while others depend on how your income is structured. Knowing where you stand can help you decide whether to adjust compensation, retirement contributions, or even business expenses.

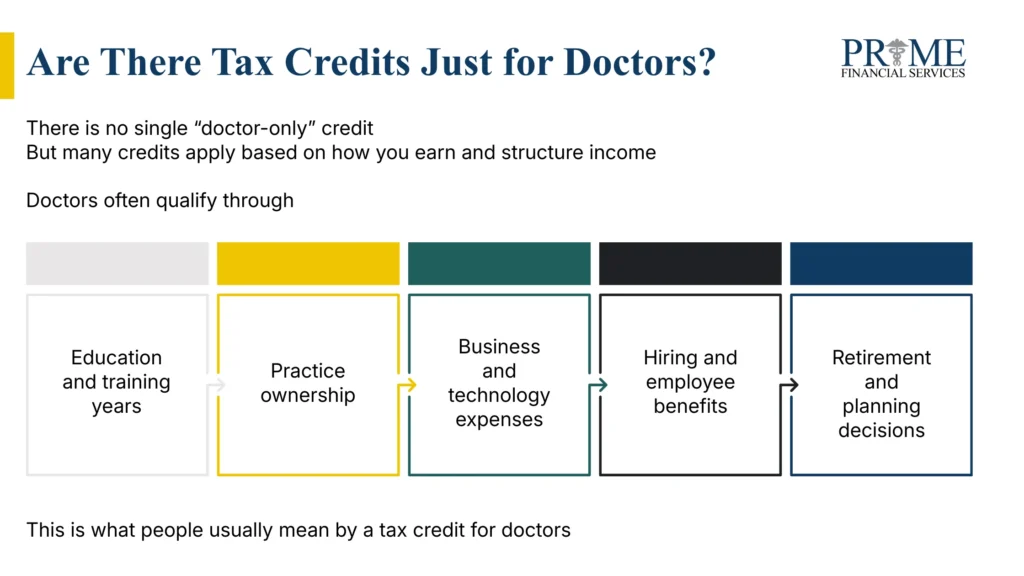

What is the tax credit for doctors?

There is no single universal credit designed exclusively for physicians. Instead, doctors often qualify through a mix of professional, business, and personal credits. When people ask about a tax credit for doctors, they are usually referring to education-related credits, energy efficiency incentives, or credits tied to practice ownership and employment structure.

For example, doctors who run or co-own practices may qualify for credits related to technology upgrades, employee benefits, or retirement plan setup costs. Physicians working in underserved areas may also benefit from state or federal programs that reward service in high-need communities.

Income level and eligibility

One area that surprises many doctors early in their careers is how income affects eligibility. Because many credits phase out at higher income levels, understanding where you fall within the 2026 tax brackets for physicians becomes essential before making strategic planning decisions. Residents and fellows may qualify for credits that attending physicians no longer can. In certain situations, early-career doctors with lower taxable income may even qualify for the earned income tax credit, especially if they have dependents and limited outside income.

Similarly, some state-level programs offer versions of a low income tax credit that apply during training years. These opportunities often disappear once income rises, which makes timing and awareness especially important.

The misunderstood business side of credits

Physicians who own practices or work as independent contractors often overlook credits tied to operations. Technology investments, training programs, and compliance upgrades may qualify for incentives depending on how expenses are categorized.

One commonly misunderstood concept is the input tax credit, which applies more often in business and indirect tax contexts. While not relevant to every physician, it can matter for those involved in multi-location practices, lab services, or other ancillary businesses. Correct classification and documentation are essential to avoid errors and missed savings.

Common questions doctors ask

Can you write off doctors on taxes?

This question often comes from practice owners asking about hiring costs. While salaries themselves are not credits, certain hiring-related expenses and benefit programs may qualify for credits depending on jurisdiction and structure.

What is the $6000 tax credit?

This amount often circulates online without context. In reality, several credits and incentives have caps around this range depending on filing status, dependents, or business setup costs. The key is understanding which programs apply to your situation rather than chasing a number.

What is the $2500 expense rule?

This usually refers to safe harbor rules for deducting certain business expenses. While not a credit, it can influence how expenses are treated and whether they support eligibility for other incentives.

What is the most overlooked tax break?

For doctors, it is often retirement-related credits or early planning incentives tied to new practices or partnerships.

What is the medical practice tax loophole?

There is no magic loophole, but there are planning strategies. Proper entity structure, timing of income, and benefit design can create meaningful savings when done correctly and compliantly.

Planning ahead for 2026

Looking ahead to tax credits 2026, the biggest advantage will belong to physicians who plan early. Credits often require action before the tax year ends. Waiting until filing season usually means missed opportunities.

Strategic planning may include:

- Reviewing income sources such as W-2, 1099, and practice distributions

- Timing major purchases or upgrades

- Evaluating retirement plan options

- Coordinating personal and business finances

These decisions are easier to make when guided by professionals who understand the medical field.

Some physicians may need more time to claim credits using a tax extension in 2026.

Final thoughts

Taxes will always be part of a physician’s financial reality, but confusion does not have to be. Understanding how credits work, which ones apply to your career stage, and how planning decisions affect eligibility can significantly change your outcomes.

Whether you are a resident, practice owner, or nearing retirement, the right guidance can help ensure that you are not leaving savings on the table. With the right structure and support, tax planning becomes less about stress and more about clarity and control.

For over seven decades, Prime Financial Services has focused on helping medical professionals handle exactly these kinds of challenges. As a third-generation firm, they work with physicians from residency through retirement, helping them build long-term wealth while addressing student loans, tax complexity, and practice growth.

Their work goes beyond numbers. By providing financial education through seminars for residency programs, fellowship programs, and private practices, they help doctors make informed decisions earlier in their careers. Tax planning is integrated with debt planning, insurance, investments, retirement strategies, and even business creation, so nothing operates in isolation.

More than 70 percent of client assets are built together over time, reflecting a long-term partnership rather than one-off advice.